✓ Compare companies and quotes ✓ Read reviews ✓ Be more aware ✓ Rank insurance companies

Advertiser disclosure

Your trust matters to us. Always.

We believe everyone deserves access to clear, honest, and unbiased information when it comes to insurance decisions. While we don’t include every provider or product available, we work hard to offer guidance that’s well-researched, accurate, and helpful completely free of charge.

So how do we keep the lights on? We may earn compensation from some of the companies we feature or link to. This can influence which products appear and where they’re placed on our site. However, it doesn’t affect our editorial standards. Our reviews and recommendations are based on thorough research, real-world insights, and a commitment to helping you make informed choices. No partner can pay to receive a favorable review.

Some of the products on this page come from partners who may compensate us when you click on their links or take specific actions. This helps us keep our content free. That said, our opinions are our own and based on independent analysis.

Shopping for health insurance is one of the most overwhelming tasks you’ll ever face, a swirling maze of deductibles, copays, networks, and fine print that can leave anyone dizzy. Yet understanding how to compare health insurance quotes can save you thousands each year, and even more importantly, ensure you and your family have the right coverage when you need it most. Whether you’re buying individual insurance through the ACA marketplace, seeking short-term plans, or getting coverage directly from insurers, this guide will help you unpack what matters when comparing quotes. By the end, you’ll know how to interpret benefits, avoid overpriced plans, and make confident decisions about your healthcare future.

Key Takeaways:

Premiums for individual health plans average $450–$700/month, but subsidies under the ACA can dramatically reduce costs for lower- and middle-income buyers.

The out-of-pocket maximum is as important as the monthly premium when comparing quotes; many “cheap” plans carry $9,000+ annual limits.

Networks can make or break your plan: confirming your preferred doctors and hospitals accept your insurance is crucial.

Choosing between HMOs, PPOs, and EPOs impacts flexibility, costs, and provider access.

Comparing plans yearly can save thousands, especially if your income, family size, or health needs change.

What is Health Insurance, and Why Is It Important?

Simply put, health care insurance is a financial deal between you and an insurance company. You pay a monthly fee, and in exchange, the insurer assists in paying some amount for your health care, which can be a doctor’s visit, a hospital stay, medicines, preventive care, etc. Research indicates that approximately 92% of U.S. citizens had health insurance coverage in 2023, with early‑2024 figures showing a very similar level of around 91.8% insured as of the first quarter. Many people wonder, ‘How much is health insurance a month?’ and this varies significantly depending on the plan and provider.

It should be noted that health care insurance acts as a buffer so that you do not have to pay all the amount without incurring a high level of credit risk. In the absence of insurance, even for sick people with ordinary colds, a simple treatment or even an impromptu visit to the ER tends to be expensive.

For example, a simple bone repair would set you back a few grand, whereas more complex things like operations or other ailments that require constant doling out could run you into hundreds of thousands.

Buying insurance assures you that you are insured and not likely to shoulder some of these financial burdens when medical emergencies occur.

Types of Health Insurance Plans

Selecting the most appropriate health care insurance plan is an individual decision, as every plan has its own benefits and disadvantages. What is important is that the option you choose should match your health requirements and availability of funds.

Plan Type

Coverage Details

Key Considerations

Health Maintenance Organization (HMO)

In-network care is mandatory, and preventive services are given priority.

Lower premiums, but you’ll need referrals to see specialists.

Preferred Provider Organization (PPO)

Includes both in-network and out-of-network care, offering greater flexibility.

Higher flexibility to choose providers, but premiums are generally higher.

Exclusive Provider Organization (EPO)

Similar to an HMO, but with fewer restrictions on seeing specialists.

No coverage for out-of-network providers, except in emergencies.

High Deductible Health Plan (HDHP)

Features low premiums but higher deductibles, making it suitable for healthy individuals.

Often paired with an HSA to cover out-of-pocket costs.

Each plan type has its unique trade-offs. For example:

HMO plans: These plans often have the lowest premiums but require you to stay within a network of providers. You’ll also need referrals to see specialists, which can limit your choices.

PPO plans: These plans provide more freedom to see doctors both in and out of the network, but they come with higher premiums and out-of-pocket costs.

EPO plans: EPOs offer a balance between affordability and flexibility, although you must use in-network providers for most services.

HDHPs: High Deductible Health Plans are ideal for individuals who don’t expect to need frequent medical care. They pair well with a Health Savings Account (HSA), where you can save pre-tax dollars for medical expenses.

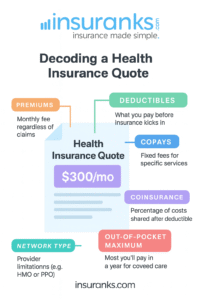

What Goes into a Health Insurance Quote?

Many people mistakenly think health insurance quotes are just a price tag, but they’re a detailed breakdown of the financial obligations you face under the plan. The monthly premium, which you pay regardless of whether you use services, is the most visible component. However, equally important are the deductible (the amount you must pay before most benefits kick in), coinsurance (your percentage of costs after meeting the deductible), copays (flat fees for specific services), and the annual out-of-pocket maximum, which caps your total spending for covered services each year.

Another critical factor is the network. HMOs typically require referrals and limit you to in-network providers, resulting in lower premiums but less flexibility. PPOs offer a wider choice but higher costs, while EPOs sit somewhere in between. Networks can vary even within the same insurer, so a Blue Cross plan in one state could include your preferred hospital, while the same insurer’s plan in another state might not.

Prescription coverage details are a must-read section of every quote. Plans categorize medications into tiers, each with different copays or coinsurance, and the difference between tiers can cost hundreds a month if you rely on brand-name drugs. Finally, mental health and specialist benefits should be scrutinized. While all ACA-compliant plans cover mental health, the number of covered visits, prior authorization requirements, and therapy copays can differ dramatically between quotes.

How to Choose the Right Health Insurance Plan

Choosing the right medical insurance requires more than simply looking at the premium costs. There are several aspects you will have to consider to ensure that the plan you select suits your health concerns and finances.

Factor

Why It Matters

Monthly Premium

This describes how much one has to pay in a month, doing so maintains the insurance in place. It is very important to make sure that the premium is tied with the other aspects, such as the deductible.

Deductible

This is the amount that has to be met before the insurance begins paying any bill. A higher deductible may be disadvantageous to some people especially those who expect to use health care services regularly.

Co-pays and Coinsurance

These are your share of the costs after meeting your deductible. If you regularly visit doctors, choosing a plan with lower co-pays might save you money.

Provider Network

Ensure your preferred doctors, specialists, and hospitals are in-network to avoid out-of-pocket costs for out-of-network care.

Out-of-Pocket Maximum

This is the highest amount that a member will have to spend within a period of one year. This also means that when a person reaches this limit he or she will not have to pay for costs anymore because insurance will cover these at a hundred percent.

When it comes to evaluating the benefits available in different plans, one could ask the following questions: Are there particular doctors that you use rather frequently? Are there any particular hospitals or healthcare facilities where you want services?

If that is the case, ensure that such providers are available under the plan’s arrangement. For instance, do you often head to the doctor’s office for treatment of a chronic disease? You may need to consider plans that have lower prescription co-pays

Updated Costs and Trends for 2025

According to the most recent Health Insurance Marketplace data, the average premium for an unsubsidized individual ACA plan in 2025 is approximately $560 per month, with family plans averaging $1,440 per month. While ACA subsidies can reduce premiums by thousands annually, many middle-income families earn just above subsidy cutoffs and pay full price. This makes it more important than ever to compare quotes to avoid overpaying.

Out-of-pocket maximums on ACA-compliant plans in 2025 have increased to $9,450 for individuals and $18,900 for families, up from $8,700/$17,400 in 2023. High-deductible health plans (HDHPs) used with Health Savings Accounts (HSAs) remain popular among healthier individuals who can afford risk, but buyers must ensure they have enough savings to cover the steep deductibles, many of which now exceed $7,500. Short-term health plans, still available in many states despite tighter federal regulations, often advertise premiums as low as $120/month but come with severe limitations, like excluding pre-existing conditions or capping annual benefits at $100,000.

These numbers highlight why comparing plans annually is critical. Rate increases vary widely by insurer and region, and each year brings new plan designs that may better match your changing needs. For those on fixed incomes or transitioning between jobs, marketplace navigators and insurance brokers can help find plans that balance affordability and comprehensive benefits.

Experts and Real People Weigh In on Comparing Quotes

Industry professionals agree that comparison shopping is the most effective way to save on health insurance. Louise Norris, a licensed broker and health insurance analyst for Healthinsurance.org, said in a January 2025 interview: “Too many people stick with the same plan year after year, unaware of better options on the marketplace. In many cases, they could save hundreds monthly simply by updating their application and checking for new plans in their area” (Healthinsurance.org, Jan 2025).

Real-world insights from Reddit’s r/HealthInsurance subreddit echo this advice. One poster in February 2025 shared how their family saved thousands a year by switching from a PPO to an HMO. While another cautioned about focusing only on premiums and ending up stuck with a deductible of thousands of dollars.

These expert and consumer voices illustrate how comparing quotes each year isn’t optional; it’s vital to avoiding unnecessary costs and surprise bills.

How Much Does Health Insurance Cost: Best Health Insurance Companies and Rates

Here’s a comparison of some of the top medical insurance providers in the U.S., with their starting rates and key features:

Insurance Provider

Starting Rates (Individual)

Key Features

Best For

Blue Cross Blue Shield

$450/month

Nationwide coverage, PPO, and HMO options

Comprehensive coverage with an extensive network

Kaiser Permanente

$350/month

HMO-focused, high-quality preventive care

Individuals seeking coordinated, in-network care

Cigna

$400/month

PPO plans with global coverage

Frequent travelers needing flexible networks

Aetna

$420/month

Affordable HDHPs and HSAs

Those looking for affordable premiums and tax advantages

UnitedHealthcare

$475/month

Wide network, many plan options

Individuals who want a broad range of coverage options

Compare Health Insurance Quotes Online

Get all the best quotes from leading providers in a click of a button!

Tips to Save on Health Insurance

Here are a few strategies you can use to save on health insurance without compromising on quality:

Compare Plans Online: Using online tools, one can compare and check out many providers at once. This allows someone to be able to make a better choice based on what they offer and their budget.

Look for Subsidies: If you belong to a certain income group, the government may provide you with subsidies that you can use to lower the premiums. This is made possible by health insurance.

Consider a High Deductible Health Plan (HDHP): If on the other hand, sickness is not a regular occurrence to you hence doctor’s services are less required, then that would be the ideal time to choose the HDHP option as it reduces the monthly premium rate.

Open an HAS: If in this case, you go for the HDHP then an HSA (Health Savings Account)must be opened which operates in such a way that a certain amount of money can be reserved for health services before tax.

Bundle Insurance Policies: Some insurers offer discounts if you bundle your health

Assess your coverage needs: Every year, you should evaluate your healthcare needs to find out if you require extensive medical insurance coverage. Based on the outcome, you can adjust your current coverage.

How often should I compare my health insurance options?

Every year. Even if you love your current plan, premiums and benefits can change annually, and new plans may better fit your needs or budget.

Can I switch plans outside of open enrollment?

Only if you have a qualifying life event, such as losing job-based coverage, moving, getting married, or having a baby. Otherwise, you’ll need to wait for the next open enrollment period.

What’s the difference between a PPO and HMO plan?

A PPO lets you see specialists without referrals and often covers some out-of-network care, but it costs more. An HMO requires referrals from your primary doctor for specialists and usually excludes coverage for out-of-network providers, but comes with lower premiums and out-of-pocket costs.

The Final Diagnosis

Health insurance doesn’t have to be a headache. By taking time to understand the real costs behind the premium, comparing quotes from multiple sources, and checking networks, you’ll avoid nasty surprises and find a plan that protects both your health and your finances. Don’t let confusing jargon or outdated plans leave you vulnerable, empower yourself to make smarter choices, so you can focus on what truly matters: living a healthy, worry-free life.

Ofir is the founder and CEO of Insuranks. He established Insuranks in 2019 from scratch and has been running educational insurance websites since 2009 on a mission to help businesses...See full bio.

Do you have U.S. insurance expertise/experience? Would you like to become a voice at Insuranks, help businesses and individuals, and showcase your authority online? Write us!

Disclosure: Insuranks.com is an independent educational comparison service and an advertising-supported publisher.

Some of the companies/offers that appear on the website are from our partners which we may receive compensation from.

This may influence which companies/offers we write about and where and how it appears on the site. However, this does not impact our assessments.

We solely highlight companies, products, and offers that can help you make smarter insurance decisions.